Top 50 Rational Formula Stocks 6/20/25

Highlighting Espey Manufacturing $ESP

Each week, I share the top-ranked companies from my Rational Formula ranking system. It’s inspired by the logic behind Greenblatt’s Magic Formula, but built with far greater depth, evaluating companies across 96 factors. The system looks for accelerating fundamentals, efficient capital allocation, expanding margins, and reasonable valuations, with a focus on consistency and improvement across multiple time frames. The goal is to generate a list of high-probability opportunities before they attract broader attention. I also highlight one company each week, sometimes as a deep dive, sometimes just an introduction. That write-up appears below the rankings.

Top Ranked Companies

(All market caps in millions — CAD for Canadian tickers, USD for U.S.)

1. Acorn Energy, Inc. — ACFN:USA — $44.2M USD

2. Altigen Communications, Inc. — ATGN:USA — $14.9M USD

3. Andrew Peller Ltd. — ADW.A:CAN — $210.4M CAD

4. Astec Industries, Inc. — ASTE:USA — $898.8M USD

5. Aveanna Healthcare Holdings, Inc. — AVAH:USA — $934.5M USD

6. BK Technologies Corp. — BKTI:USA — $185.1M USD

7. Biotricity, Inc. — BTCY:USA — $11.3M USD

8. Burnham Holdings, Inc. — BURCA:USA — $110.9M USD

9. Butler National Corp. — BUKS:USA — $101.4M USD

10. CareCloud, Inc. — CCLD:USA — $106.7M USD

11. CareRx Corp. — CRRX:CAN — $184.4M CAD

12. Conrad Industries, Inc. — CNRD:USA — $82.8M USD

13. CoreCard Corp. — CCRD:USA — $223.6M USD

14. Crawford United Corp. — CRAWA:USA — $171.6M USD

15. DAVIDsTEA, Inc. — DTEAF:USA — $20.1M USD

16. Decisive Dividend Corp. — DE:CAN — $143.7M CAD

17. Enhabit, Inc. — EHAB:USA — $472.6M USD

18. Espey Manufacturing & Electronics Corp. — ESP:USA — $107.3M USD

19. EverQuote, Inc. — EVER:USA — $885.1M USD

20. Firan Technology Group Corp. — FTG:CAN — $292.4M CAD

21. Geodrill Ltd. — GEO:CAN — $161.5M CAD

22. Greystone Logistics, Inc. — GLGI:USA — $36.1M USD

23. The Gorman-Rupp Co. — GRC:USA — $926.4M USD

24. Imaflex, Inc. — IFX:CAN — $65.7M CAD

25. InfuSystem Holdings, Inc. — INFU:USA — $129.8M USD

26. Innovative Solutions & Support, Inc. — ISSC:USA — $216.8M USD

27. Kamada Ltd. — KMDA:USA — $415.2M USD

28. Karooooo Ltd. — KARO:USA — $1,460.6M USD

29. Kaltura, Inc. — KLTR:USA — $313.1M USD

30. Magellan Aerospace Corp. — MAL:CAN — $1,046.5M CAD

31. Medical Facilities Corp. — DR:CAN — $303.0M CAD

32. Nature's Sunshine Products, Inc. — NATR:USA — $270.6M USD

33. Nephros, Inc. — NEPH:USA — $38.0M USD

34. NetScout Systems, Inc. — NTCT:USA — $1,719.4M USD

35. NetSol Technologies, Inc. — NTWK:USA — $33.5M USD

36. NowVertical Group, Inc. — NOW:CAN — $51.7M CAD

37. Ooma, Inc. — OOMA:USA — $339.2M USD

38. Optex Systems Holdings, Inc. — OPXS:USA — $71.4M USD

39. Optical Cable Corp. — OCC:USA — $22.4M USD

40. Paul Mueller Co. — MUEL:USA — $286.7M USD

41. Perfect Corp. — PERF:USA — $205.7M USD

42. Pyxus International, Inc. — PYYX:USA — $128.0M USD

43. RCM Technologies, Inc. — RCMT:USA — $172.9M USD

44. RF Industries Ltd. — RFIL:USA — $53.2M USD

45. Thermon Group Holdings, Inc. — THR:USA — $906.6M USD

46. TOMI Environmental Solutions, Inc. — TOMZ:USA — $21.2M USD

47. Upland Software, Inc. — UPLD:USA — $52.7M USD

48. Yellow Pages Ltd. — Y:CAN — $155.5M CAD

49. Zedge, Inc. — ZDGE:USA — $53.8M USD

50. Zoomd Technologies Ltd. — ZOMD:CAN — $114.2M CAD

This Week’s Highlighted Company: Espey Manufacturing ESP

What Espey Does

Espey Manufacturing builds ruggedized power electronics for demanding environments—transformers, converters, and custom power systems installed on U.S. Navy ships, military aircraft, locomotives, and heavy industrial vehicles. These low-volume, high-spec components must survive shock, vibration, saltwater, extreme heat, and long-term abuse.

Most of Espey's products end up inside platforms where failure means catastrophe, like destroyers, submarines, or aircraft. Their gear must work reliably for decades and can't be swapped for cheaper parts without full regulatory approval.

Everything is designed, manufactured, and tested in-house at their 151,000-square-foot facility in Saratoga Springs, New York. This vertical integration appeals to customers by simplifying procurement, shortening timelines, and lowering risk. Espey serves as both design partner and single-source manufacturer for critical systems.

The customer base is concentrated but high quality: Raytheon, Lockheed Martin, Boeing, and the U.S. Department of Defense directly, customers that don’t churn suppliers easily. Some commercial exposure exists in industrial vehicles and rail, but defense forms the business core. The model is durable and built on long-term contracts. Once ESP is selected for a platform, it typically stays for the life of the system due to high qualification standards and regulatory friction.

Long-Cycle, Government-Driven Demand

I estimate that 80-90% of Espey's revenue follows the slow-moving gears of U.S. defense spending rather than consumer demand or GDP growth.

The sales cycle unfolds in stages. Government increases funding, often tied to geopolitical concerns, naval modernization, or specific programs. Then prime contractors and platform builders place orders, appearing in Espey's backlog. Revenue follows 6 to 24 months later in chunks based on production milestones or delivery events.

Using percentage-of-completion accounting, revenue hits in stages over extended periods. Once work enters the backlog, it reaches the income statement 95% of the time. This provides visibility: Espey's current $82.9 million funded backlog covers roughly 1.75x trailing revenue, supporting the next 6–8 quarters even without new orders.

Espey also disclosed a broader backlog figure of $138 million in its most recent press release, compared to the $82.9 million funded backlog reported in the 10-Q. The difference reflects newly booked contracts that haven’t yet been funded or scheduled for delivery. These are orders not yet recorded under GAAP backlog rules but they are very likely to make it into the funded backlog number soon.

Much of Espey’s work is front-loaded. The designing, prototyping, tooling, and testing of components to meet rigorous military specs requires significant upfront time and cost. But once Espey is validated on a platform, it typically becomes the sole supplier for that component over the life of the program. The longer the platform runs, the more leverage the company gets on those initial investments. That’s why long-cycle programs like Navy destroyers and submarines are attractive: they allow Espey to earn strong margins for years without redoing the upfront work.

New contracts often show up in the financials before they appear in revenue. Espey typically incurs costs upfront—materials, labor, tooling—before contract milestones trigger revenue recognition. That means a quarter can look weaker than it really is if multiple new programs are ramping up at once. Cash gets deployed early, and margins can dip temporarily. Over time, as production stabilizes and revenue milestones are met, the economics normalize. This makes individual quarters lumpy and misleading even when the long-term performance is stable.

Management operates with a long-term view rather than optimizing quarter-to-quarter performance.

Business Quality

Espey’s operating model checks a lot of the boxes we look for in a durable small industrial. Gross margins have steadily improved over the last two years, rising from the low 20s to 35–36% today. That margin expansion reflects a shift from legacy fixed-price contracts (which got hit by inflation) to better-priced, more recent work.

The company is vertically integrated. Design, manufacturing, and testing all happen in-house at their Saratoga Springs facility. That reduces procurement risk for customers and gives Espey tighter control over cost, quality, and lead time. It also makes the company hard to replace. For a mission-critical supplier working in defense and rail, those factors matter more than scale.

The balance sheet looks good: $38.5 million in cash and marketable securities, no debt, and essentially no stock-based comp. The company doesn’t dilute. Even with capital-intensive equipment and testing needs, they’ve managed to self-fund everything.

Insider alignment is decent, around 6% direct ownership plus a 9.6% ESOP. Management communicates sparingly, rarely issues press releases, and doesn’t seem interested in managing the stock price. But they’ve tripled operating income under the current CEO, raised the dividend, and kept backlog elevated for seven straight quarters.

This is a business built for long timelines and heavy qualification cycles.

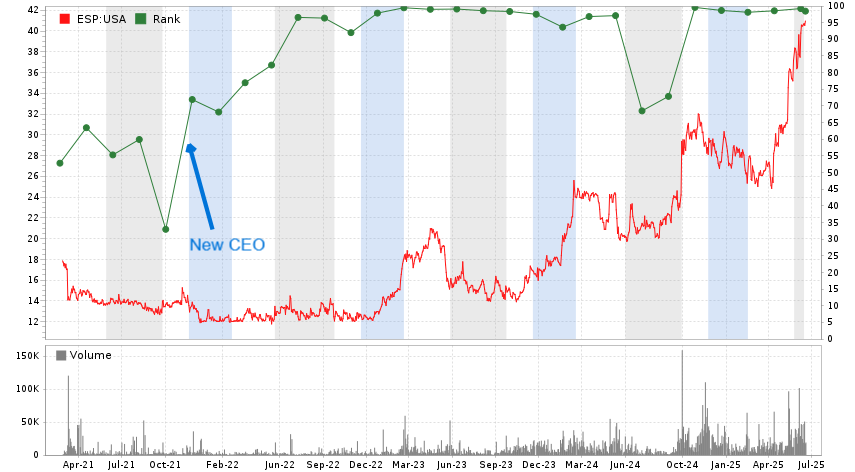

The CEO Shift and What's Changed

David O'Neil became CEO in January 2022 after over two decades as CFO. Since then:

Backlog has stayed above $80 million for seven straight quarters

Gross margins expanded by 10–12 points

Operating income tripled in two years

The Navy contributed $7.4 million for high-power testing expansion

Espey reinstated its dividend and raised it within a year

Execution looks better and more focused. Orders are steadier, margins are stronger, and the financials now match the conservative balance sheet. This is the kind of outcome the CEO’s compensation package is designed to reward.

The Investment Case

Espey currently trades at an enterprise value of ~$76.5 million (market cap of $115M less ~$38.5M in cash and securities), against trailing metrics of:

TTM revenue: $47.1 million

Operating income: $12.2 million

Free cash flow: ~$10 million (adjusted for working capital swings)

Gross margin: 35.7%

This puts it at:

EV/EBIT: ~6.3x

EV/FCF: ~7.7x

EV/Revenue: ~1.6x

These multiples are low for a capital-light, cash-rich, defense-aligned niche supplier. By comparison:

Public peers in niche defense electronics (e.g. CPI Aero before going dark, or smaller segments inside L3Harris or Curtiss-Wright) often command EV/EBIT multiples between 10–14x depending on margin and backlog visibility.

High-margin, low-growth industrials without defense exposure often trade at 8–12x EBIT if cash-rich and stable.

Espey has modest reinvestment needs. Its returns on tangible capital have improved dramatically with margin expansion:

ROIC is hard to pin precisely due to cash drag and lumpy capex, but EBIT over invested capital (excluding cash) is easily 20%+ in the current run-rate, strong for an industrial.

There’s little dilution risk, no need for acquisitions to drive growth, and no leverage to obscure returns.

Management expects revenue to grow again in fiscal 2025, but net income to dip due to product mix (fulfilling older—fixed-price before inflation—contracts) and a one-time pension charge. That creates a near-term headwind for margins, but doesn’t alter the longer-term picture.

The Optionality: DDG-X

Espey currently supplies custom power systems for the Navy’s existing destroyer classes, DDG-51 (Arleigh Burke) and DDG-1000 (Zumwalt). These platforms are aging, and over the next decade, they’re set to be replaced by the Navy’s next-generation destroyer: DDG-X. This shift represents the most important procurement transition in Espey’s addressable market, and potentially the biggest opportunity the company has seen in decades.

DDG-X is being designed to support next-gen weapons, propulsion, and radar. These systems require much more electrical power and thermal control than previous classes, conditions Espey is specifically built to handle.

In 2023, Espey received a $7.4 million funding contribution from the Navy to expand its high-power testing capabilities. This was a co-investment in infrastructure, suggesting the Navy sees Espey as a key supplier in this next era of ship design. The expansion allows Espey to qualify higher-voltage, higher-wattage systems, capabilities aligned with the Navy’s technical goals for DDG-X.

Management hasn’t disclosed whether Espey is already in the DDG-X supply chain, and awards aren’t expected until late FY2025 or later. But the signs are encouraging:

The Navy is funding facility upgrades

Espey has a multi-decade track record supplying naval platforms

Gross margin and backlog have improved even before the new destroyer class is awarded (Prime contractors and the Navy favor reliable, low risk suppliers for mission-critical systems. Delivering consistently on existing programs shows execution capability)

If Espey is selected, revenue would follow the usual defense timeline: first a backlog surge, then revenue spread across 10–20 years as ships are commissioned and built. This would meaningfully extend the company’s visibility, increase scale, and potentially justify higher valuation multiples.

There’s no guarantee of a win, but Espey is positioned as a credible incumbent.

Risks and Constraints

Customer concentration is the biggest risk. Most of the business ties back to the U.S. Navy and a handful of contractors. If Espey fails to win DDG-X or similar long-cycle awards, revenues could fade as current platforms wind down.

Production is limited to a single facility. While recently upgraded, any surge in demand could strain throughput or require capex.

The company has a track record and recent funding, but DDG-X awards remain competitive until signed.

Final Note

This isn’t a 10x. Not anytime soon, anyway. But with margins at a decade high, cash piling up, and a major new destroyer platform on the horizon, it’s not hard to see how this could double from here.

The stock has mostly ranked near the top of the Rational Formula ranking system since late 2022 (Right after the new CEO took over), which reflects steady operational progress. Backlog already supports the next 6–8+ quarters, and the DDG-X decision could extend that by another decade.

In a market where capital is getting more selective and geopolitical risk is rising, Espey could do well. It’s a stable, well-run defense supplier with some optionality, and despite the recent run up it’s still priced at what looks like a significant, though not enormous, discount.

If you made it this far, you’re either unusually thorough or dangerously curious. Either way, you might as well subscribe.

Disclosure: I own shares of Espey Manufacturing (ESP) at the time of publication. I may buy or sell shares at any time without notice.

Disclaimer: This content is for informational and educational purposes only. It does not constitute investment advice, an offer, or a recommendation to buy or sell any security. All investors should do their own due diligence or consult a licensed financial professional before making investment decisions.

Hi Ryan, fantastic writeup. This stock also came up on my screen, spent yesterday and today digging into it, seems like a good opportunity.

Out of curiosity, were you able to speak with management? They don't put out a lot of information, so I was impressed seeing how much new information you had! Good job, keep up the good work Ryan.

Fantastic stuff as usual, Ryan!

Would love to see a bonus episode on which UK & European stocks rank highly.